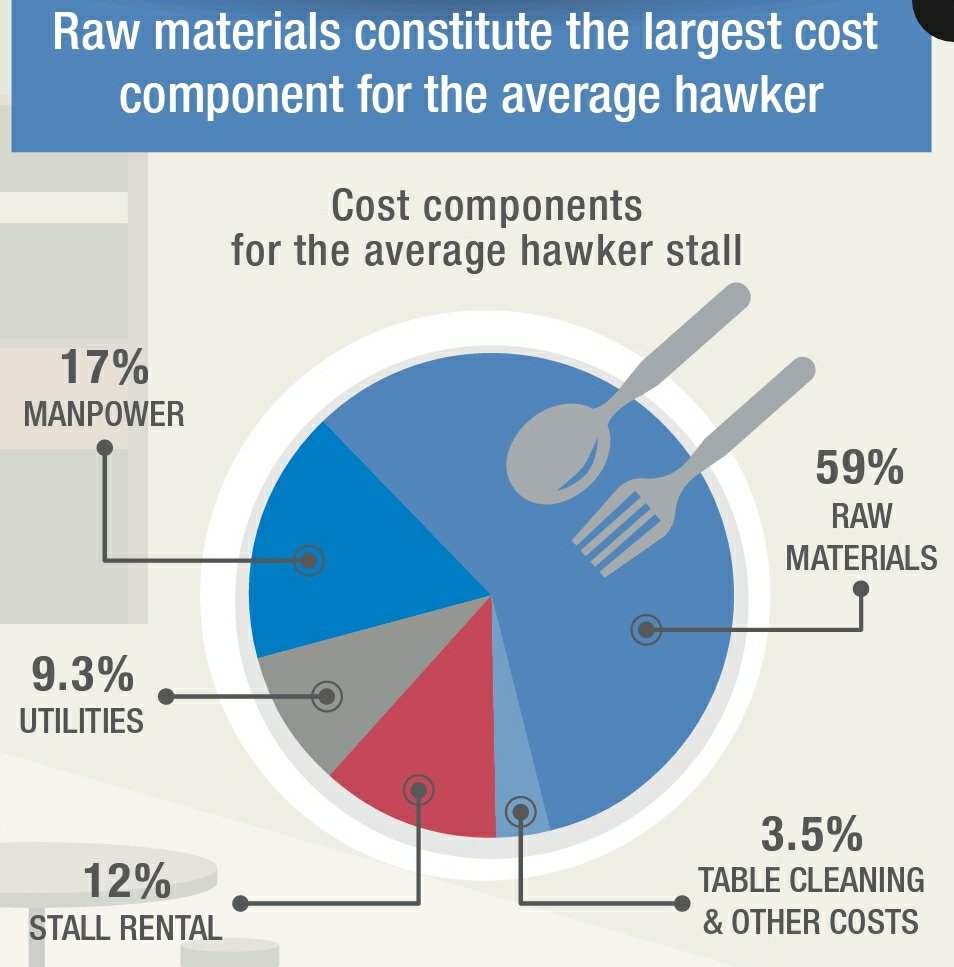

Cai png is economic rice

Cai Png is a dish of economic rice. The term “economic” refers to the affordable dish of rice with several selection of veggies and/or meat.

Unfortunately, there is no price label on the varieties of veggies or meat (aka dishes). Regulation is lax. Hence, regular customers are accustomed to becoming smarter, i.e., they are able to identify expensive dishes (in order to avoid them).

Bait or trap?

Sometimes, meat fried with a batter (aka fritter) can make it difficult to identify the dish. It is thus prudent to ask the stall owner or helper for the identity of the meat, else you will be charged higher for fish, prawn, squid or other seafood. In addition, any veggies fried with anchovies, small shrimps, or other seafood may also be charged as meat or “seafood”, and you end up paying higher price for the dish than normal veggies.

It is unfortunate that you are misled to think that you are ordering vegetables, while in actuality you are not. It may be frustrating when you have to argue with the stall owner. It brings back memory of pre-Jover Chew’s Sim Lim Square time when regulation and standards were poor there (ref. 3).

It is a trap

A cai png with fish at AMK Mayflower hawker centre that cost $11 was a trap (ref. 1). It was a TRAP because the dish was not priced and customer assumed that the dish in a hawker centre should be reasonably priced. Unfortunately, there was no price label or pricing table. It is understandable that the customer was shocked and upset.

The owner had justified the price of her mackerel at $8 per slice by suggesting that her fish was bought “fresh” versus frozen. Such justification is completely irrelevant and illogical. What’s next, Premium Wahyu beef fritters fried with veggies that would cost $10 per scoop? If she had the audacity to price her fish slice at $8, she should be more responsible to include a price tag there to prevent potential misunderstanding, especially when cai png at hawker centre is hardly as expensive as hers.

Alas, it is understandable that she had more motivation to lay the “trap” at her stall for gullible patrons to step than to act responsibly (by displaying the price). Unfortunate for her, in the age if social media, her act can become viral (i.e., highly shared in social media).

Include price to build trust

If you want to build cuatomer trust, ensure your business practices are ethical. Else, you will become viral and untrustworthy, regardless of how much you justified your act (especially when it made lesser sense after the reasoning).

Reference

- Cai Png with fish from AMK Mayflower hawker centre costs S$11 (https://mothership.sg/2022/06/economy-rice-expensive-singapore/)

- Hawker who sold viral $11 cai png with fish explains why it is so expensive (https://goodyfeed.com/viral-11-cai-png-responds/)

- Jover Chew, former boss of Mobile Air jailed 33 months for conning customers, also fined $2000 (https://www.straitstimes.com/singapore/courts-crime/jover-chew-former-boss-of-mobile-air-jailed-33-months-for-conning-customers)